How States Can Take Control of Disaster Funding in 2026

Hurricane making landfall in Key West, FL

With the future of the Federal Emergency Management Agency (FEMA) in flux and a movement underway to shift the burden of disaster response and recovery to state and local governments, two questions become inevitable: Who will pay for the rising cost of emergency management? And how?

Trillions of dollars have been spent over nearly six decades to establish a system and infrastructure with FEMA as central authority to oversee the federal government’s disaster response and recovery efforts. This infrastructure also supports a well-established network of state and local government emergency management agencies. However, all signs now point to a new model that will redefine the federal government’s long-held roles and responsibilities, leaving state and local governments without a clear roadmap for how the transition will be managed. In many ways, this would revert to a pre-Stafford Act dynamic, and many states are not prepared for such a shift.

If the federal government follows through with its promise to significantly reduce the scope of FEMA or eliminate it altogether, state emergency management agencies will need to come up with a new playbook to handle large-scale disasters.

Which brings us back to the central question: who’s going to pay for all of this? Fortunately, several options are available to states who seek to minimize the impact of the federal government’s retreat.

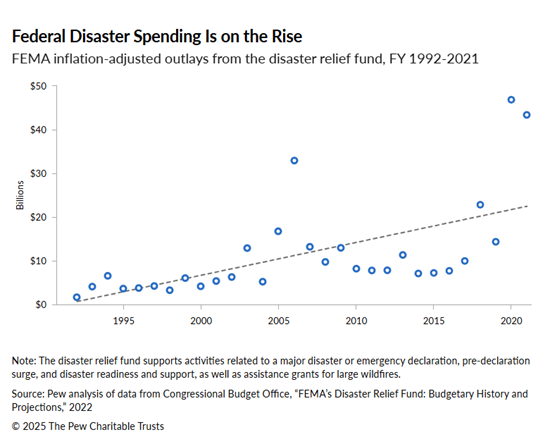

Chart displaying the increase of federal disaster spending over the past 30 years

Risks vs. Resources

Not all states carry the same amount of risk and liability where natural disasters are involved. Some states are susceptible to hurricanes while others may be vulnerable to tornadoes, wildfires, earthquakes, or other catastrophes. This contributes to a dynamic landscape of state and local government preparedness, with some areas requiring more robust response and recovery capabilities than others.

Similarly, not all states have the same resources at their disposal when it comes to supporting emergency management departments. For states who have grown reliant on federal assistance for disaster response and recovery, the potential elimination of FEMA could have calamitous effects unless they identify alternative sources to fund hazard mitigation and emergency management efforts.

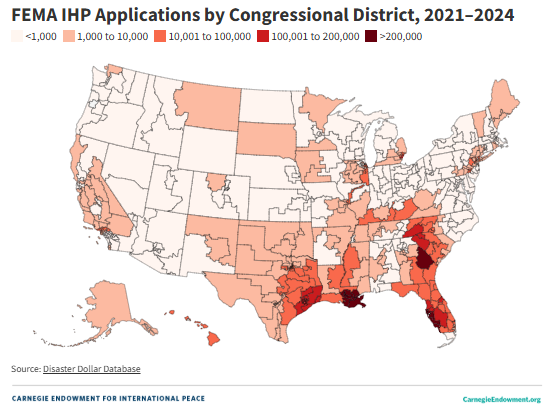

Chart showing the average number of households per state seeking assistance from FEMA’s Individuals and Households Program (IHP).

A Potential Roadmap for the Future

A recent report from the Pew Charitable Trusts may serve as a blueprint for states that are unsure of their path forward. Based on a series of studies from 2018 to 2022, the report outlines how states respond to natural disasters and provides recommendations to minimize the budgetary impact of response and recovery.

The suggestions made by the Pew authors can be summed up by three key principles: Measure, Manage, and Mitigate.

Measure

Effective emergency management begins by understanding potential risks. Historical data provides a baseline to reference when predicting future disasters. States must begin by compiling that data to gain a better understanding of their environment and vulnerabilities so they can forecast the potential cost of future disasters.

Manage

All states should have a “rainy day” fund that can be tapped in the event of emergency, and nearly all do, but many utilize inconsistent funding sources, which can leave these state-run accounts vulnerable during an economic downturn. Having a dedicated source of funding and tightening control over how and when those accounts can be tapped must be a top priority for state legislatures, especially for states that don’t yet have a disaster recovery fund.

Mitigate

The first line of defense against disaster is hazard mitigation. By taking a more proactive approach, investing in emergency preparedness, and providing incentives for citizens and businesses to reduce risk, states save money on future disaster response and recovery operations.

The biggest takeaways from this report are the specific, actionable recommendations laid out nicely for state governments to help prepare for a future that includes a streamlined version of FEMA, or no FEMA at all.

Those recommendations are:

Collect comprehensive data

Produce meaningful disaster spending reports

Budget proactively

Define state responsibilities

Invest in mitigation and resilience

Maximize investments from nonstate sources

The primary option available to states, which is not emphasized much in this report, is for states to permanently invest in the systems that already exist in each state’s emergency management agency that support FEMA’s Public Assistance (PA) Program. Every state has (or should have) a state PA officer, charged with managing the flow of PA grants from FEMA to their state agencies and local government partners. It will be much more challenging to transition through this period of change for those states who do not have vibrant PA capabilities at the state level. Conversely, these recommendations will be much easier to implement for those states that already have PA expertise.

Several homes show significant damage following a storm in Chattanooga, TN

Alternative Funding Options States Should Consider

The larger conversation about FEMA’s future is occurring at the same moment that disasters are growing in frequency, severity, and cost. From 2020 to 2024, major disasters cost a combined $746.7 billion – nearly as much as the entire 2010s ($994.7 billion). Researchers at the University of Chicago created a statistical model suggesting that US disaster damages from 2026 to 2030 will top $500 billion (90%+ chance), with a 54% chance that those damages will exceed $1 trillion.

There is a very real risk that disasters will bankrupt state governments, but that does not need to happen. With proper planning and a prudent financial approach, states can weather a worst-case scenario without relying solely on federal funding assistance or exhausting their disaster recovery fund. To do so will require a more modern approach that leverages all available financial tools to fund mitigation, response, and recovery programs.

State & Regional Risk Pools

State risk pools could operate similarly to catastrophe risk pools, which are already in use around the world. The premise is rather simple and nearly identical to the idea behind insurance: everyone contributes to a shared pot, and if disaster strikes, the impacted party can draw from the pooled resources to cover their expenses.

Establishing a regional model using state risk pools would ensure that no individual state shoulders the full burden of a disaster completely on their own. However, it could be a tough sell to get states that rarely experience major disasters to contribute to a shared fund with more vulnerable neighbors.

Catastrophe Bonds

Catastrophe bonds were created following Hurricane Andrew – at the time the costliest hurricane to make US landfall. Hurricane Andrew led to the failure of eight insurance companies and caused other insurers to reexamine their risk exposure in coastal areas.

In response, insurance companies created a new financial instrument called a catastrophe bond, which is a high-yield, insurance-linked debt instrument that provides lucrative returns for investors over the bond’s term while offering coverage for insurers in the event of a major disaster. Essentially, investors are betting against a particular disaster occurring over a specific period (usually three or five years). Returns tend to be higher than the market average; however, if catastrophe strikes, the principal is used to fund disaster operations and the investor’s capital is forfeited.

By leveraging these types of securities, state governments would have access to immediate capital following a major disaster, which would allow them to quickly begin the recovery and rebuilding process. For investors, catastrophe bonds offer a high-risk/high-reward portfolio option that is proving to be popular. In 2025, the market for catastrophe bonds reached a record high with $61.3 billion in outstanding capital and $25.6 billion in new issuances, which was a 45% increase over 2024.

Reinsurance Markets

When an event happens that causes insurance claims to spike (like after a hurricane, for instance), insurance companies can find themselves in a position where they do not have the necessary funds to cover all claims. This is where reinsurance comes into play. In a nutshell, it is insurance for insurance companies. Having reinsurance increases the overall capacity of an insurance company by allowing them to transfer a portion of their risk to reinsurers in exchange for a cut of the premiums paid by customers.

As the cost of disasters has grown, insurers have seen their profits decrease to the point that some have decided to stop providing coverage to residents of certain states or areas. Several strategies have been suggested to combat this phenomenon, from public-private partnerships to federal- and/or state-supported reinsurance schemes. Florida has the Reinsurance to Assist Policyholders (RAP) Program, while multiple bills have been introduced in the US Congress to create a national disaster risk reinsurance program and catastrophe reinsurance fund.

Trees burn during the Lava Mountain Fire in Shoshone National Forest, WY

In this new paradigm, all options must be on the table and state governments should consider using a combination of approaches to ensure they have adequate funding for disaster relief. Furthermore, tying participation in risk pools or reinsurance programs to mitigation efforts should also be part of the overall strategy. Study after study has shown that spending on mitigation is a far more efficient and effective use of funds than supporting a damage-repair-damage-repair cycle.

As disasters increase in frequency and severity, states face increased pressure from the federal government and municipalities to shoulder more of the burden of disaster relief. It’s imperative that state agencies use the tools at their disposal to compile and understand the data, use a prudent financial strategy to fund and manage emergency response efforts moving forward, and dedicate resources to mitigation projects that will drive down the future cost of disasters.